What is a foreign firm in our complex, inter-connected world? Professor Sara McGaughey from the Department of Business Strategy and Innovation, and colleagues Pascalis Raimondos and Lisbeth la Cour, ask this question in an article published in the world’s premier International Business Journal, with intriguing results.

The authors show the importance of taking into account both direct and indirect ownership links to the ultimate foreign owner when categorising a firm as ‘foreign’ in a host economy, with implications for managers, policy makers and scholars of international business.

Large multinational enterprises (MNEs) increasingly utilize detailed and complicated ownership structures, sometimes seeking to hide direct ownership patterns for tax and financial reasons. Complexity in MNE structures is further driven by the increasing growth and fragmentation of production that results in MNEs constantly reconfiguring their international value chains, and by modalities of growth such as mergers and acquisitions, joint ventures and alliances between firms.

But having a direct foreign owner does not necessarily make a firm ‘foreign’, since a domestic entity may in turn own that foreign owner (a phenomenon called ‘round tripping’). Likewise, having an immediate domestic owner does not necessarily make a firm ‘domestic’ because the domestic owner may in turn be foreign controlled.

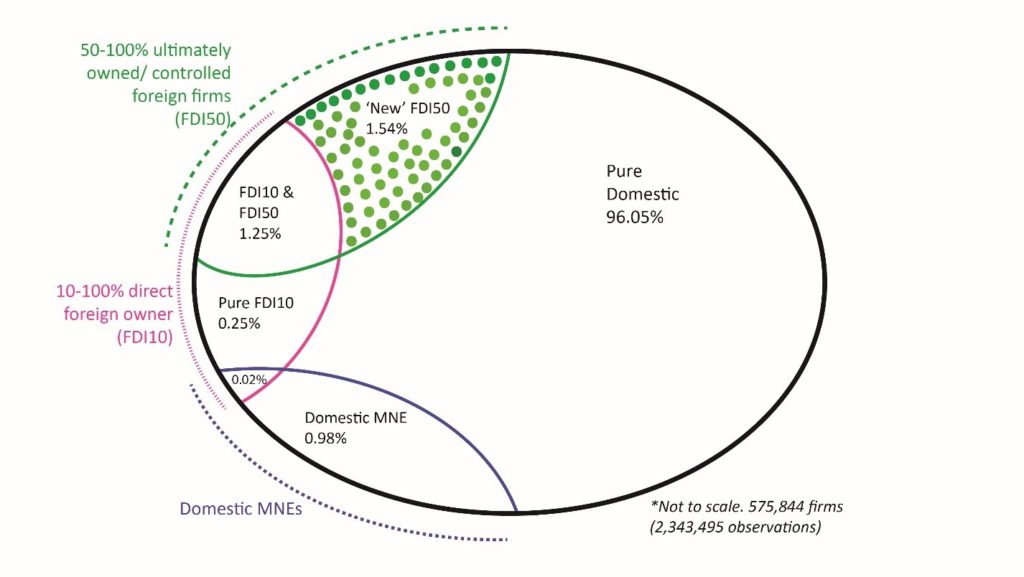

Using a firm-level panel dataset of 575,844 manufacturing firms (2,343,495 observations) across 20 European countries, the authors highlight two distinct ways in which a foreign firm is identified: (1) the conventional use of a low threshold of 10% equity by a direct (i.e .immediate) foreign investor, and (2) a control-based definition, with a high 50% equity in each link in the chain to the ultimate foreign owner.

Intuitively, the authors expected that the conventional foreign direct investor definition would pick up more foreign firms than the control-based definition with its higher ownership threshold. However, they find there are just as many indirectly controlled foreign firms without an immediate foreign owner as there are foreign firms captured under the conventional direct investor definition.

These ‘new’ foreign firms would be classified as domestic firms in studies that use only immediate foreign direct investor data. Yet it is these indirectly controlled foreign firms that are found to have the strongest positive effect on the productivity of domestic firms of all foreign firms.

The findings raise non-trivial concerns of mismeasurement in any study using only direct ownership data to identify foreign firms, with implications for managerial practice and government policy directed at foreign direct investment.

Illustration of ownership data.

Please click here to read the full “Foreign influence, control, and indirect ownership: Implications for productivity spillovers” article published in the Journal of International Business Studies, written by Sara McGaughey (Griffith University), Pascalis Raimondos (Queensland University of Technology), and Lisbeth la Cour (Copenhagen Business School).