By Professor Sara McGaughey (Griffith Business School) and Professor Pascalis Raimondos (QUT)

BREXIT is the perfect natural policy experiment, i.e. an unexpected shock that allows one to map out the effects that government policy has on businesses. What happened on 23 June 2016 in Great Britain — when more than 30 million people participated in a referendum that resulted in 51.9% voting in favour of the UK exiting the EU — was not anticipated by the markets. The November 2018 developments have reinforced that we still do not know what is going to happen.

We won’t actually know the precise effects for many years, but we can be sure that researchers have already started thinking about it. Several ‘event’ studies have already emerged that examine how share prices have been affected by the 2016 vote.1 These studies show that, while there are always losers and winners, uncertainty overall hurts businesses.

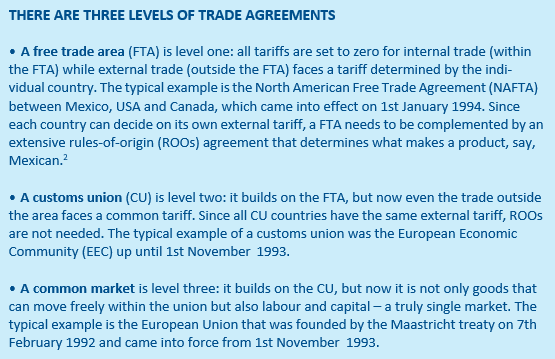

In order to understand where the BREXIT uncertainty comes from, let’s first go back to some fundamentals on trade agreements.

On top of these trade agreements, countries can agree to enter a common monetary policy and thus a common currency. An example of this is the eurozone, established 1 January 1999. Further collaboration in terms of fiscal policy (i.e. common taxes) brings countries closer towards a federation where basically there is only one country left.

The BREXIT referendum was about the withdrawal of Britain from the EU and, as such, the UK’s potential withdrawal from both the customs union and the common market. Since the BREXIT vote two years ago, the negotiations between Britain and the EU have been about finding the best solution for both partners.

The possible options for Britain were the following:

Option 1: Moving from level 3 to level 2

If Britain wants to leave only the single market (no free migration into Britain), it could try to negotiate a customs union agreement similar to, for example, what Turkey has with the EU. Sorting out the visa issues of the millions of British people living in the EU (and vice versa) would be the focus. National borders would only be important for the movement of people, as goods would still be traded freely between Britain and the EU.

Option 2: Moving from level 3 to level 1

If Britain wants to leave both the customs union and the single market, then it could try to negotiate an FTA agreement, similar to what Norway or Switzerland has with the EU. On top of the visa issues, the ROOs would have to be negotiated with the EU. National borders would be important both for people and for goods as both must have a ‘country of origin’.

Option 3: ‘No deal’

Finally, if Britain wants to have no trading agreement whatsoever with the EU, then it could trade under the so-called WTO rules that every member of the World Trade Organization has to follow. Britain will be like Australia when it comes to trading with the EU — no ROOs need to be specified.

While the standing-alone option (#3) is the one that Britain can decide unilaterally, it is also the option where the economic losses will be largest. Firms will have little incentive to locate in the UK and will prefer to relocate within the large EU market. The HM Treasury estimated that the losses of ‘standing alone’ could be as large as a 7.6% drop in the UK’s GDP.3

Option #2 of an FTA makes border control for trading products essential. However, reintroducing a physical border that separates Northern Ireland from the Republic of Ireland is unlikely. The 1998 Good Friday Agreement (also known as the Belfast Agreement) between the UK and Ireland remains a core constitutional text of the two nations. Among other things, it commits the nations to North-South cooperation and guarantees the absence of the ‘hard border’ that would be necessary for a FTA between the EU and UK. The Agreement effectively constrains how the UK can leave the EU, and requires the UK and Ireland to jointly consider the impact of BREXIT on cross-border issues.4

Option #1 is the least costly, given that borders are not important for goods trading within a customs union. Indeed, this is also the solution that the EU recently agreed with the Prime Minister Theresa May in November, and which the British Parliament voted down this month.

However, while this solution allows Britain to control its migration flows, to stop paying to the EU, and to make its own rules and regulations, it locks Britain into a set of trading rules over which Britain will have no influence. Such an outcome is clearly not a long-term solution and will not remove the uncertainties that businesses face — it will actually aggravate them!

This article originally appeared in German-Australian Business News magazine and has been republished with the authors’ permission.

Footnotes:

1 See Dhingra et al. (2017), Breinlich et al. (2018), Bloom et al (2018), Davies and Studnicka (2018). 2 Without ROOs Mexico can decide that all Chinese goods enter Mexico at a very low tariff, and then they are transported into the US as Mexican goods, thereby paying zero border taxes. Mexico gets all the tariff revenues while US gets zero tariff revenues for the goods that American consumers want to buy from China. 3 See HM Treasury (2016). 4 See Green (2017) for a detailed discussion.

References:

Bloom, N., S. Chen, and P. Mizen (2018). ‘Rising Brexit uncertainty has reduced investment and employment’, VoxEU at https://voxeu.org/article/rising-brexit-uncertainty-has-reduced-investment-and-employment Breinlich, H., E. Leromain, D. Novy, T. Sampson, and A. Usman (2018). ‘The economic effects of Brexit – Evidence from the stock market”, CEPR Discussion Paper 13147.

Davies, R. B. and Z. Studnicka (2018). ‘The heterogeneous impact of Brexit: Early indications from the FTSE’, European Economic Review 110: 1-17.

Dhingra, S., H. Huang, G. Ottaviano, J. P. Pessoa, T. Sampson, and J. Van Reenen (2017). ‘The costs and benefits of leaving the EU: Trade effects’, Economic Policy 32: 651-705. Green, D.A. (2017). ‘How Ireland is shaping Britain’s post-Brexit trade’. Financial Times, 15 December.

HM Treasury (2016). ‘The Long-term Economic Impact of EU Membership and the Alternatives’, London: HMSO